The financial services industry is barely recognizable from two decades back. Advancements in technology have ushered in a new era in banking. From smartphones to big data, the landscape has evolved in ways almost unimaginable to previous generations.

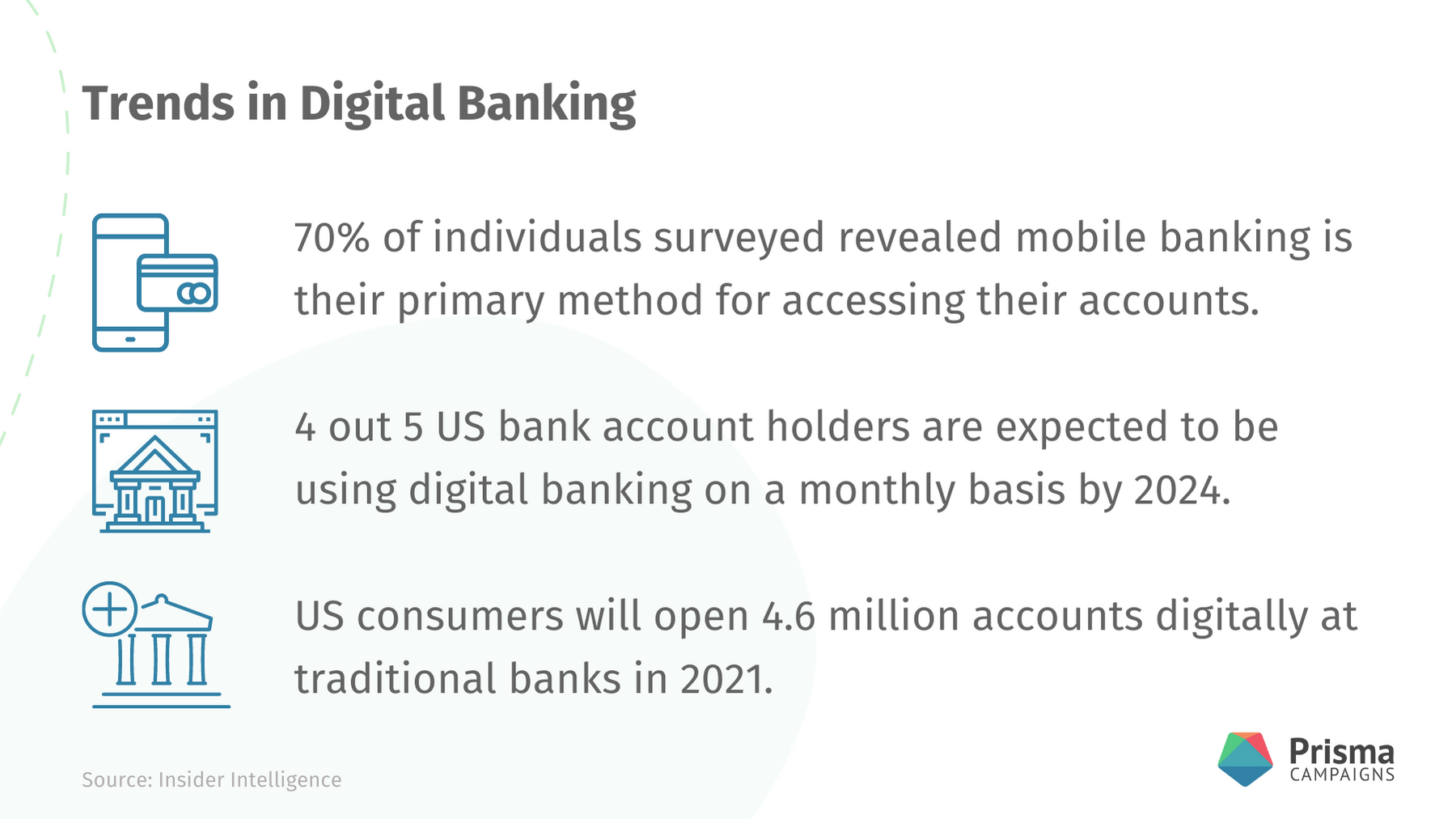

In 2021 US consumers are expected to open an impressive 4.6 million accounts digitally at traditional banks. By 2024, 80% of US bank account holders are expected to be engaging in digital banking on a monthly basis.

Clearly, consumers are willing to engage with technology, and so must be the institutions that serve them. Traditional banks aren’t exempt. They must continue to adopt digital tools that consumers increasingly expect.

Let’s take a closer look at some of the most significant technological developments and what they mean for the industry today.

Mobile: Pocket-Sized Banking

After social media and weather, mobile banking apps are among the most popular downloads you’ll find in your favorite app store. According to a survey from Insider Intelligence, nearly 9 out of 10 US respondents indicated they use mobile banking channels. Further, an incredible 70% revealed mobile banking as their primary way to access their accounts. And when it comes to millennials, virtually all of them (97%) conduct regular banking primarily through their smartphone.

The effects of COVID-19 have only intensified this growing trend. The Financial Brand revealed 30% of FI customers increased their mobile banking use since the onset of the pandemic.

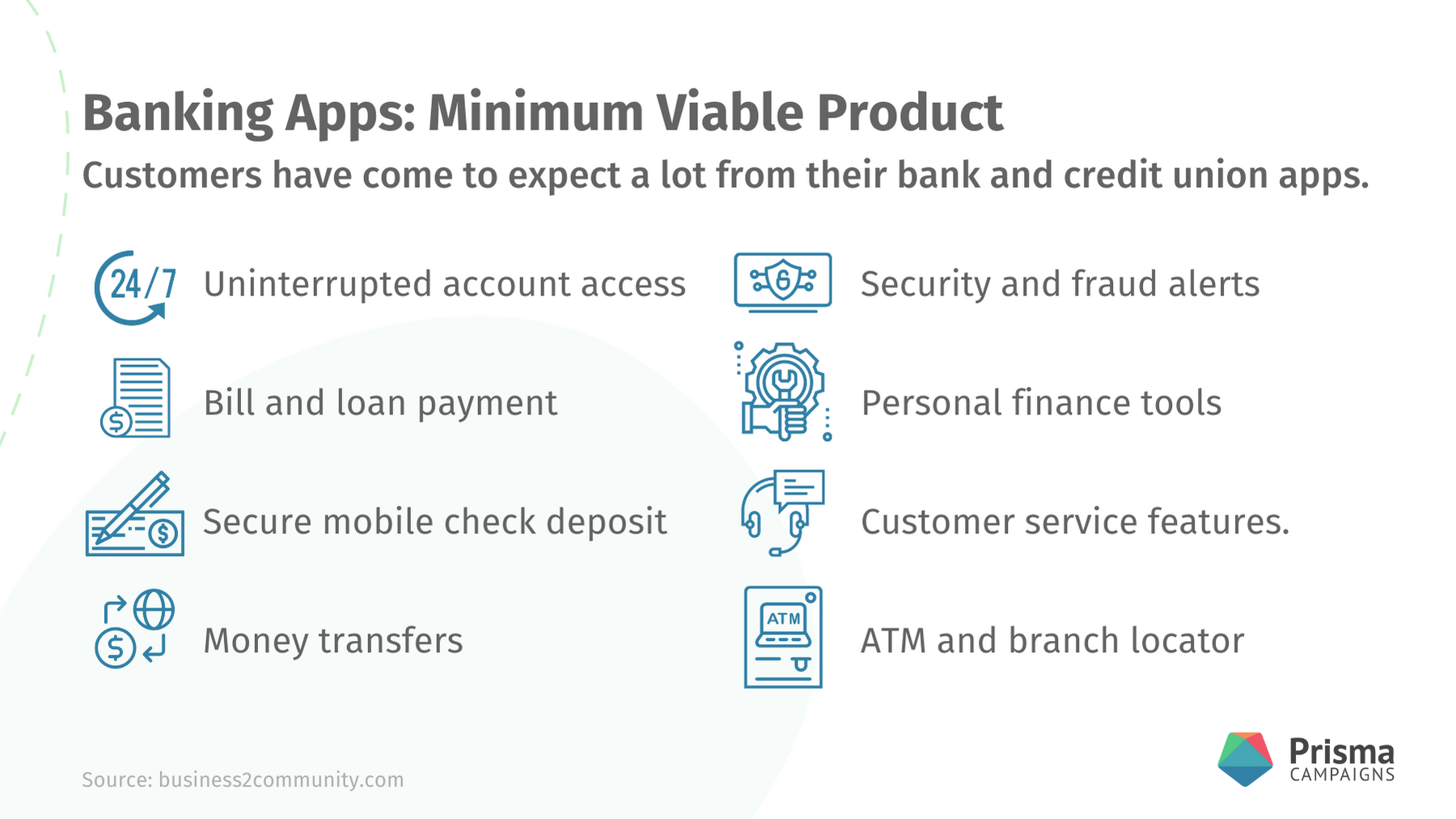

Clients, especially younger ones, are attracted to mobile solutions. Banks must ensure their apps not only offer a variety of services, but are user-friendly, fast, and look good. After all, aesthetics matter.

A 2020 Marqueta survey revealed 21% of respondents ranked an easy-to-use mobile app as the most important feature a bank can provide, while only 15% placed in-person experience at the top.

That’s not to say that in-person experience isn’t important, far from it. For those customers obtaining their first mortgage, or a small business receiving a loan, the in-person experience can be invaluable. Rather, this tells us that banks and credit unions shouldn’t bet on digital or physical alone. Customers value both experiences, and emphasizing one at the expense of the other will likely prove costly from a customer retention perspective.

Harnessing the Power of Big Data

90% of marketers are now using artificial intelligence (AI) to provide customers an optimal and rewarding user experience. Of course, years of data points for thousands of customers are only valuable once synthesized.

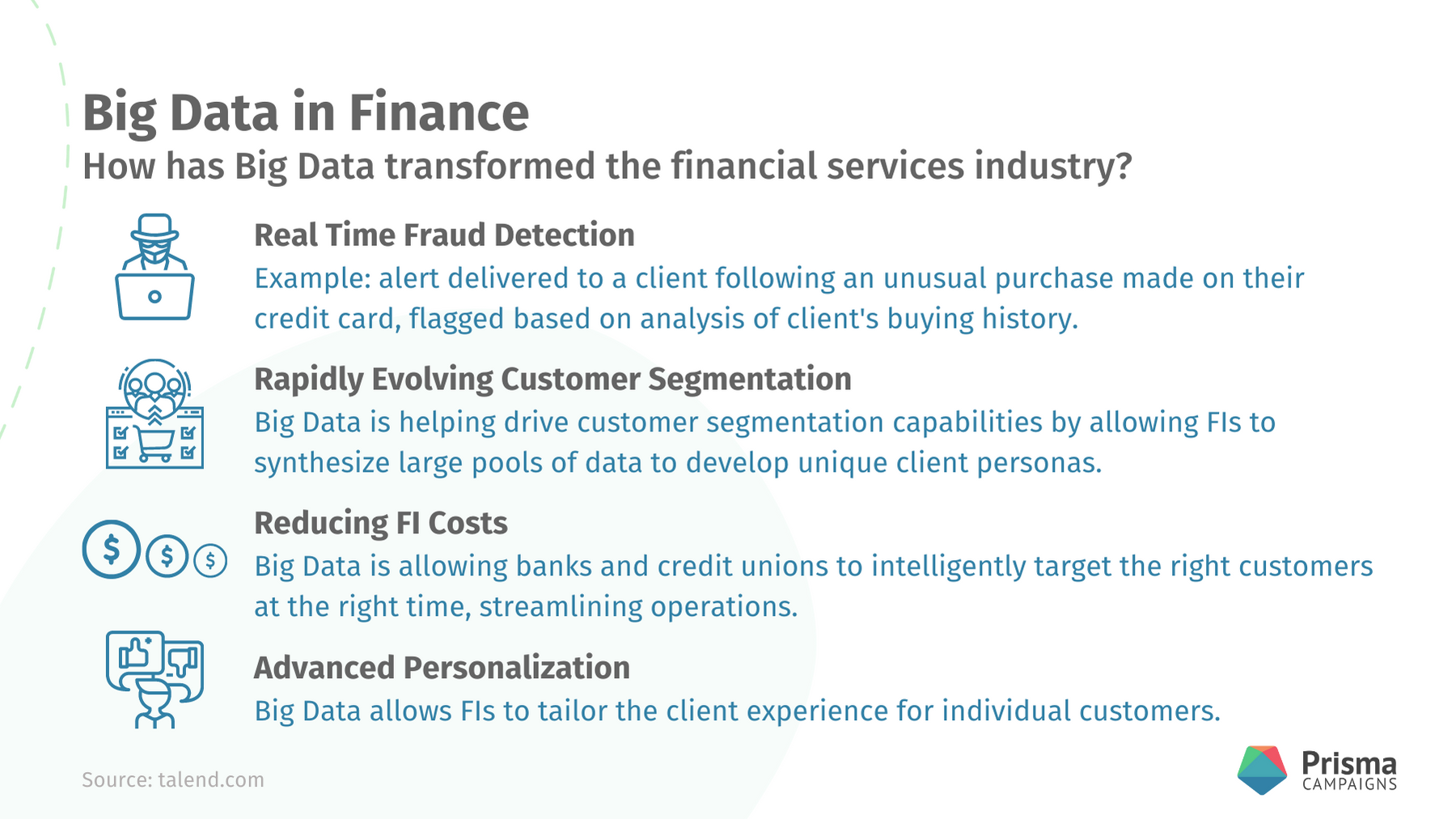

Luckily, the large swaths of data banks have collected over decades can now be analyzed and refined to provide valuable insights. Technological advancements have made it possible for computers to comb through what was once an impossible task for mere mortals. Not only that, these computers are now doing it at breakneck speeds, allowing for creative uses, like real-time security alerts for clients.

Unfortunately, companies are much better at collecting data than actually interpreting it. According to a Veritas Global Data Report, on average, the data collected of the companies profiled fell into one of three buckets:

-

52% was considered dark data where the actual value was unknown.

-

33% was deemed redundant, obsolete, and trivial (ROT) data (verified as useless).

-

15% was considered useful, business-critical data.

The good news? When properly organized and managed, banks can convert dark data into valuable, business-critical data. Data that will ultimately help deliver a unique customer experience.

The Big Data frontier is only just beginning. Still, it’s already proving beneficial in numerous areas in the financial landscape.

Curating a Custom Customer Experience

Personalized experiences are becoming table stakes for companies. Impersonal messages are increasingly treated with contempt by clients. In a world where customers are bombarded with spam, targeted emails are essential for building trust, driving adoption, and ultimately, retention.

Netflix has spoiled us. Those familiar with the platform know how easy it is to navigate and are likely familiar with the personalized home screen. The more you use the streaming service, the better Netflix becomes. It learns and grows with you. It recommends movies and shows based on your past behavior.

Increasingly, customers are expecting something similar from their bank. When speaking of personalization in banking, we’re referring to leveraging client details to suggest relevant products and services that match a customer’s current preferences and lifestyle.

Just like Netflix suggests a rom-com for John based on his viewing habits, a credit union might recommend a particular auto loan for Julia based on her current life stage, income, and unique history.

Banks should utilize existing digital channels customers are already frequenting rather than relying so heavily on traditional email campaigns that net few conversions. When customers are already actively visiting these digital channels for their financial needs, conversion to new products, like a credit card, is more likely.

Put another way, digital channels can help remove some of the friction associated with conversions.

If you still view your digital channel as a place exclusively for transactions, you might be leaving precious connections with your customers on the table. Using powerful software solutions like Prisma Campaigns can greatly improve the client experience, and ultimately help improve sales.

What’s Next?

With exciting new technology comes uncertainty and risk. As banks and credit unions increasingly undertake digital transformations, emphasis on security and privacy will be paramount. Newly emerging technologies, like cryptocurrency and decentralized finance (DeFi), are only beginning to make waves among traditional banks.

The pandemic has shaken up the industry, and depending on how long it persists, may change consumer behavior for the long term. While many customers still covet branch visits, the transition to digital as a core banking method seems irreversible. It’s incumbent upon traditional banks to navigate this change gracefully.

In the coming years, a key characteristic of successful FIs will undoubtedly be their openness to new technological advancements and eagerness to work with other leaders in the fintech space and elsewhere.